How (RDR) Transforms Chargeback Management

Here’s how RDR inside a payment orchestration platform like UpGate benefits both merchants and acquirers

Disputes don’t need to escalate into costly chargebacks, with Rapid Dispute Resolution (RDR), merchants can step in early and resolve cases before they become a problem. With solutions like Visa Rapid Dispute Resolution (RDR), merchants can intervene before a transaction evolves into a full chargeback, saving time, money and reputational risk.

Here’s how integrating RDR within a payment orchestration platform like UpGate offers significant benefits for both merchants and acquirers.

What is RDR and how does it work?

At its core, RDR is a next-generation technology developed in partnership with Verifi and built into Visa Resolve Online (VROL) that helps merchants resolve disputes at the pre-dispute stage, meaning before they escalate into full chargebacks. (Chargebacks911)

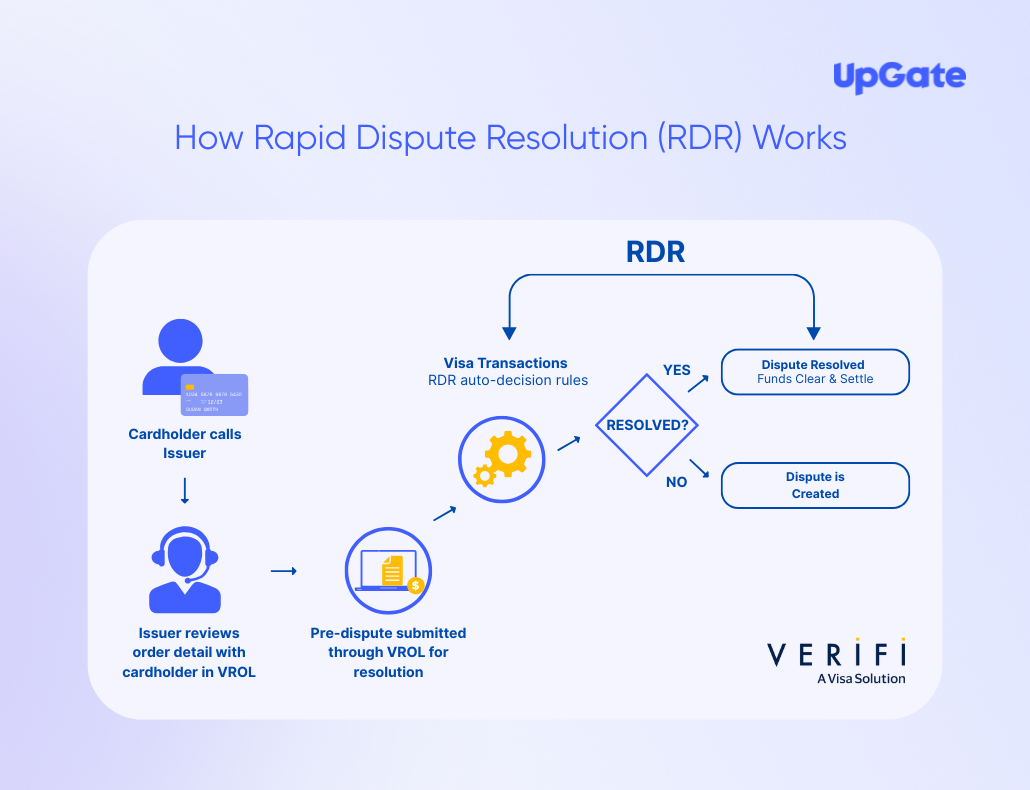

Here’s the flow:

A merchant enrols one or more Merchant IDs (MIDs)/accounts into RDR and defines a set of rules that determine which disputes the merchant is willing to accept liability for automatically.

When a dispute is initiated (by the issuer via VROL) and the merchant is RDR enabled, the system checks the case against the merchant’s preset rules.

If no rules match, the default decision is “Decline” liability → the case proceeds through the standard chargeback/dispute process.

If the rules trigger an “Accept” decision (i.e., the merchant accepts liability), then the case is resolved immediately at the pre-dispute stage, the customer is credited via VROL on behalf of the issuer and the chargeback is avoided altogether.

Once the rules are in place, the process is fully automatic, no manual refunds or intervention required from the merchant for the accepted cases.

Importantly, because the dispute is resolved before chargeback, the transaction does not count towards the merchant’s chargeback/dispute ratio (in many cases) and the merchant avoids a full chargeback cycle.

Why it matters: The benefits for merchants

Faster resolutions & less administrative burden

Resolving disputes in the “pre-dispute” phase means far less time spent chasing chargebacks, gathering evidence, responding to acquirers and issuers, and engaging in lengthy back-and-forth.

Prevention of full chargebacks & reduced cost

By stopping eligible disputes early, merchants avoid the cost associated with full chargebacks: lost revenue, processing fees, manual staff hours, logistics, representment risk and reputational damage.

Better merchant-network reputation

Since RDR-resolved cases (when accepted liability) often don’t count in the dispute ratio, your metrics improve and you’re less likely to trigger monitoring programmes such as Visa Acquirer Monitoring Program (VAMP).

Transparency and visibility

Merchants get access to better reporting and analytics around dispute patterns, volumes, automatic decisions and outcomes, enabling them to refine their rules and control the dispute lifecycle.

Lower dispute ratio and risk of enforcement

For example, recent data from Visa shows: 97% global Visa-issuer coverage of RDR and US$695 million in pre-disputes resolved. (Visa Corporate)

Why integration with a payment orchestration platform makes sense

A payment orchestration platform like UpGate is already centralising transaction routing, acquirer selection, multi-currency processing, risk and reconciliation. Adding RDR into that ecosystem brings several synergies:

Unified data flow: Dispute-related triggers, merchant rules and decision-logic sit alongside routing and payment logic, making monitoring, analytics and optimisation much easier.

Dynamic rule-sets: Merchants can define and adjust RDR rules based on transaction metadata available in the orchestration layer (BIN, geography, value, reason code, product type).

Consolidated reporting: Instead of separate dispute systems, the orchestration layer can surface RDR outcomes alongside payments and chargeback metrics, providing a single “source of truth”.

Operational efficiency: Automated “accept” decisions mean fewer manual workflows, meaning the merchant staff and the platform’s operations team spend less time handling disputes and more time on growth.

Proactive risk management: Since RDR prevents the escalation of disputes, it improves the merchant’s overall risk profile, which in turn supports better acquirer relationships, fees and scale.

Statistics & market insight

Industry commentary suggests RDR can prevent 50% to 70% of eligible Visa chargebacks when implemented effectively. (Chargeback)

One article cites that merchants implementing RDR and similar tools can stop about 70% of Visa’s chargebacks. (Chargeback)

According to Visa: 97% of global Visa issuers are covered by RDR. (Visa Corporate)

Visa reports $695 million of pre-disputes resolved via its network. (Visa Corporate)

With the launch of its dispute overview, Visa and Verifi estimated that RDR/its predecessor CDRN would cover about 57% of all card-brand disputes globally on launch, with growth expected. (verifi.com)

Note: With the recent update to VAMP rules, merchants must note that fraud-related disputes resolved via RDR or CDRN may no longer be excluded from the VAMP ratio calculation. (Chargeback Gurus)

Why for UpGate’s merchants this is a win

As a B2B payment orchestration platform, UpGate works with merchants handling complex payment flows, multiple currencies, acquirers and risk-profiles. Integrating RDR in this environment offers:

Enhanced control across multi-acquirer, multi-region processing: rather than disputes being managed in silos, you can leverage orchestration logic for rule application and dispute mitigation across regions.

Improved cost-management: With high value B2B transactions, avoiding chargebacks when they arise (especially cross-border) saves significantly more than a standard e-commerce scenario.

Better data analytics: When the orchestration layer is already capturing rich meta-data (product, customer segment, geolocation, settlement currency), your RDR rule-sets can be far more targeted and effective.

Stronger network relationships: Maintaining lower dispute ratios and clear dispute prevention workflows helps your merchants keep favourable relationships with acquirers and card networks, essential when scaling B2B operations.

Strategic value: By offering RDR as part of your value-stack you help merchants not only route payments but defend against a major cost centre (disputes & chargebacks), positioning UpGate as a more holistic payments partner.

For merchants and platforms looking to go beyond reactive dispute management and instead prevent chargebacks at the pre-dispute stage, RDR delivers a compelling tool. When embedded into a payment orchestration platform like UpGate, the advantages, from improved control, data-leverage, cost-savings and operational efficiency, become even stronger.

If you’re processing Visa transactions, grappling with dispute/chargeback volumes, or simply looking to optimise your payments stack end-to-end, integrating RDR is a strategic move.

Ready to see how UpGate can help you integrate RDR and elevate your dispute-resolution strategy? Book a demo with our team today and let us show you how you can turn disputes into strategic advantage.

Book a demo with our team today and let us show you how you can turn disputes into strategic advantage.